|

Getting your Trinity Audio player ready...

|

TL;DR: The latest fintech trends show that global success is no longer driven by product innovation alone. As the fintech market size expands and cross-border opportunities grow, most failures happen because companies underestimate operational complexity. Fintechs that scale successfully across borders do so by re-engineering fintech operations early—combining cloud-native technology, automated fintech compliance, resilient cross-border payments infrastructure, and flexible global workforce models. Strategic use of global fintech hubs and managed operations enables faster market entry, lower risk, and sustainable fintech growth in both mature and emerging markets.

Did you know that despite the fintech market size reaching USD 394.88 billion in 2025, nearly 70% of fintech startups fail navigating regulatory compliance? Surprisingly, most failures aren’t about poor products or weak market demand. They stem from companies underestimating the operational complexity of scaling across borders. Notably, nearly six out of ten international expansion attempts collapsed under cross-border compliance challenges.

The fintech industry has evolved far beyond digital payments or mobile banking. The latest fintech trends reveal a new truth: successful fintech companies don’t just innovate; they operationalize. Those that prioritize operational readiness before market entry achieve three times faster penetration rates and sustain long-term fintech growth across markets.

Related post: Why US Companies Choose Offshore Staffing in the Philippines to Scale Operations

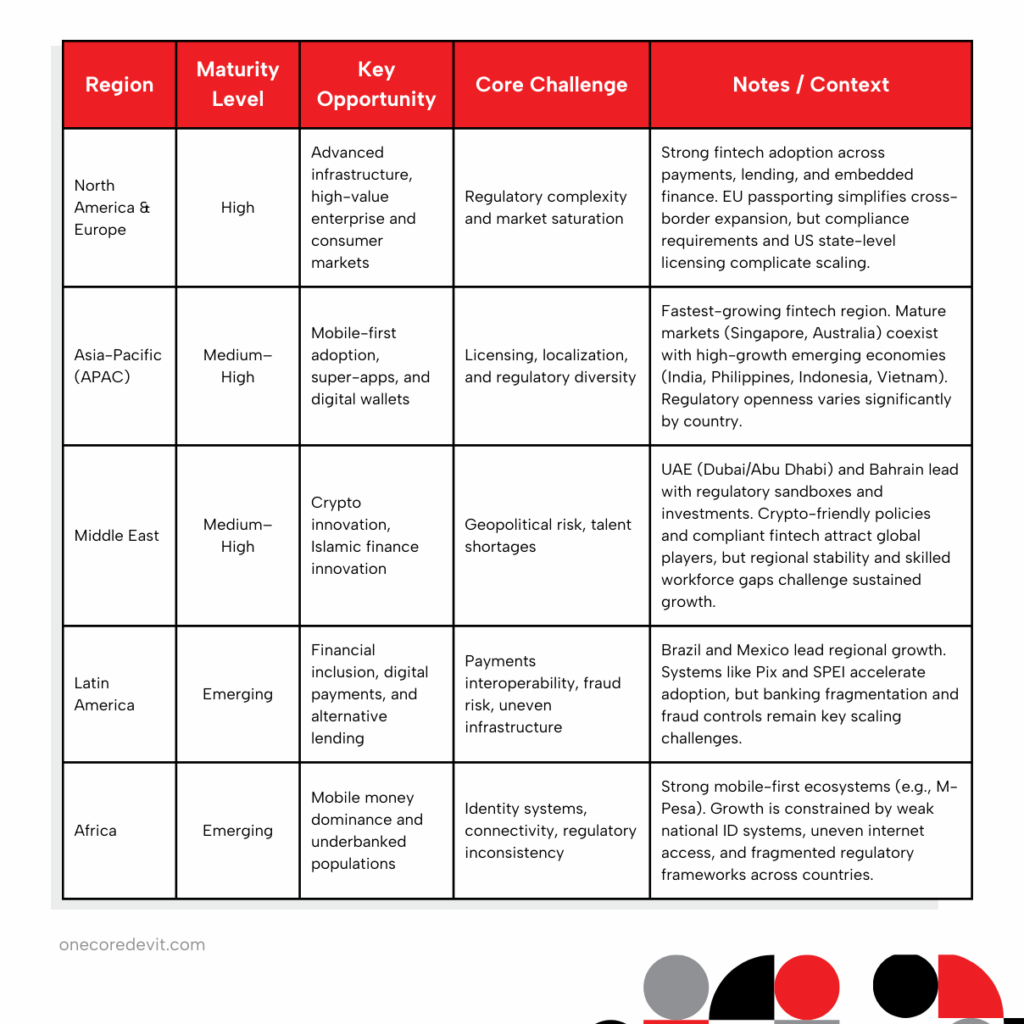

Understanding the Current Fintech Industry Landscape

The fintech industry presents unprecedented opportunities for global expansion. With mobile payment users reaching 5.2 billion worldwide and digital banking accounts reaching 1.75 billion, the market conditions have never been more favorable.

However, the landscape varies dramatically across regions.

North America and Europe represent mature markets with high regulatory complexity but significant revenue potential. Asia-Pacific offers medium-to-high maturity with massive mobile payment adoption, while Latin America and Africa present emerging opportunities with unique infrastructure challenges.

What does this mean for your expansion strategy?

The growth patterns in fintech show that successful companies tailor their operational approach to the maturity level of each region. The framework you use to enter Singapore cannot simply be applied to Nigeria, because regulatory requirements vary significantly across countries. There is no one-size-fits-all model.

While localization is a powerful driver of market penetration, it must be carefully balanced with regulatory and operational readiness to avoid compliance risks.

Here’s how market maturity differs globally:

Key Fintech Trends Driving Global Expansion

Three major fintech trends are reshaping how companies plan international growth:

1. Regulatory Harmonization Creates Expansion Corridors

Frameworks like the EU’s PSD2 directive and open banking regulations in Asia-Pacific are creating “regulatory corridors” that allow compliant fintechs to expand faster across similar jurisdictions. By leveraging these alignments, companies reduce licensing costs and avoid duplicating compliance work.

- Opportunity: Faster entry into multiple markets through aligned standards.

- Challenge: Fragmentation still exists. Data privacy and consumer protection laws vary widely, requiring operational agility.

2. Embedded Finance Redefines Operational Integration

Partnership-driven models are rising. Fintechs that build their operations to support embedded finance can integrate into non-financial businesses. These include retailers, logistics providers, SaaS platforms — for faster distribution and scalability.

- Example: Stripe powers payments for global SaaS firms, while Grab and GCash in Asia have evolved into super apps offering payments, lending, and insurance.

- Impact: Embedded ecosystems lower customer acquisition costs and create new revenue streams across borders.

3. Real-Time Cross-Border Payments Demand New Infrastructure

The shift to real-time settlement rails and blockchain-based networks is dismantling traditional correspondent banking. Central bank digital currencies (CBDCs) and initiatives like SWIFT GPI or BIS’s Project Nexus are reshaping how money moves globally.

- Opportunity: Faster, more transparent cross-border payments expand access and trust.

- Pressure: Fintechs must rebuild core payment operations to meet new standards for speed, transparency, and compliance.

4. AI and Data-Driven Operations (Emerging Layer)

Artificial intelligence is increasingly embedded into fintech operations — from fraud detection and credit scoring to personalized financial services. AI-driven compliance and customer support reduce costs while enabling scale.

- Projection: AI in fintech is expected to grow from USD 9 billion in 2025 to 41 billion by 2030.

- Operational Edge: Firms that integrate AI into risk management and customer experience gain resilience in global expansion.

5. Tokenization and Digital Assets

Blockchain tokenization lets everyday investors buy fractions of real estate, art, or private equity through digital tokens. This trend turns traditionally illiquid assets into accessible opportunities for fintechs worldwide.

- Opportunity: Democratizes high-value investments across emerging markets, blending traditional finance with digital innovation.

- Challenge: Regulatory rules vary by region, requiring careful navigation.

6. Climate/Impact Fintech (Regulatory Must)

Carbon tracking tools, green loans, and sustainability platforms help fintechs meet mandatory ESG requirements for institutional partnerships. Government sandboxes and compliance rules make this essential for global expansion.

- Opportunity: Unlocks massive sustainable finance markets and builds trust with institutional investors.

- Challenge: Standardizing sustainability data across borders remains complex.

Related post: How Filipino Professionals Excel in Outsourced Finance and Accounting

Quick Takeaways

- Operational readiness is now a primary determinant of global fintech success.

- Compliance complexity scales exponentially across borders, making automation and centralized oversight essential.

- Centralized risk and compliance with localized execution outperform fully centralized or fully local approaches.

- Modern cross-border payments require real-time, event-driven infrastructure, not legacy correspondent banking models.

- Fintechs that pair global fintech hubs with distributed, managed workforces scale faster and with less regulatory risk.

Building Robust Fintech Operations for International Markets

Scaling fintech operations globally demands far more than translating your product or opening regional offices. It requires re-engineering your organization’s operational DNA — systems, workforce, governance, and compliance — for multi-market resilience and long-term adaptability.

The challenge isn’t merely “adding new markets.”

Each market introduces unique regulatory structures, payment ecosystems, and cultural nuances that affect every part of your business — from transaction processing and customer support to data privacy and staffing models.

Smart fintech companies approach international growth like building a distributed enterprise. They design operations, talent, and infrastructure to scale together. This approach flex where local agility is needed and centralizing where consistency drives efficiency.

Centralize Risk, Localize Customer Support & Scale Workforce Intelligently

Leading fintech trends show that the most effective organizations follow a hybrid operational model:

Centralized functions:

- Risk management

- Global compliance

- Data protection

- Treasury

Localized functions:

- Customer support

- Dispute resolution

- Partnership management

This dual model ensures consistent compliance standards and policy execution while maintaining agility to serve customers in local markets.

But here’s the missing link many leaders overlook:

Workforce scalability:

Global expansion inevitably strains internal teams, especially compliance, risk, and support units.

Forward-thinking fintechs are now using managed service partners or Employer of Record (EOR) solutions to expand workforce capacity in new regions without establishing local entities prematurely.

These solutions give you the flexibility to:

- Deploy trained compliance and operations teams across time zones

- Maintain operational continuity during new market launches or audits

- Scale workforce resources up or down with market demand

- Stay compliant with local employment laws and tax regulations

This human layer complements the technology layer, creating a holistic scaling model where systems, processes, and people evolve together.

Build Technology for Global Scale

Technology is the enabler of scalable fintech operations, no longer a back-office function but the foundation of global competitiveness.

As fintech companies expand across borders, they must design systems that can evolve as fast as regulatory frameworks, payment networks, and customer expectations.

In 2026, success hinges on building technology that scales seamlessly — across markets, teams, and compliance regimes.

Future-ready fintech operations rely on four key architectural principles:

1. Cloud-First, Multi-Region Infrastructure

A cloud-first approach enables global agility.

Cloud platforms allow fintech companies to deploy infrastructure closer to customers, meet data residency and privacy compliance requirements, and dynamically scale during high-volume events like market launches or seasonal surges.

Multi-region deployment ensures:

- High availability and disaster recovery

- Regional redundancy for low-latency user experiences

- Elastic scaling that aligns infrastructure costs with transaction volume

Some advanced fintech companies are now adopting multi-cloud strategies, distributing workloads across several providers to improve resilience, avoid vendor lock-in, and comply with varied regional data policies.

For growing firms, this also supports scalable workforce management. This enables globally distributed engineering and operations teams to collaborate within unified cloud environments.

2. API-First and Microservices Architecture

Modern fintech trends favor API-first and microservices-based architectures that emphasize modularity and interoperability.

Instead of monolithic applications that slow innovation, microservices enable teams to build, deploy, and scale services independently.

An API-first architecture allows fintechs to:

- Integrate seamlessly with local payment networks, RegTech platforms, and banking APIs

- Expand into new markets quickly by connecting new regional partners or vendors

- Maintain consistent user experiences globally, even when backend systems differ

This composable structure supports faster innovation, reduced downtime, and localized customization — critical when operating in markets with differing regulatory or banking ecosystems.

3. Automated Compliance and Real-Time Monitoring

As fintechs expand, compliance automation becomes non-negotiable.

Manual processes that worked in one jurisdiction can’t sustain multi-market operations. Instead, automation ensures continuous compliance while reducing human error and administrative load.

Next-generation RegTech integrations automate:

- Real-time regulatory monitoring and alerts

- AML/KYC verification pipelines

- Automated suspicious activity reporting (SARs)

- Periodic audit and filing automation across markets

These systems detect anomalies and regulatory changes proactively, allowing compliance teams to act quickly.

This automation doesn’t replace people; it scales their impact, enabling leaner compliance teams to oversee broader global operations.

4. Event-Driven and Real-Time Data Architecture

Scaling cross-border payments requires infrastructure that can process millions of transactions in real-time without compromising on security or visibility.

Modern fintechs are adopting event-driven architectures that use message queues to handle high-throughput, low-latency workloads.

Event-driven systems enable:

- Instant transaction reconciliation across currencies

- Proactive fraud and anomaly detection

- Faster reporting and customer updates

- Seamless multi-region coordination across compliance, payments, and customer support

Measuring Fintech Growth in New Markets

Measuring fintech growth globally requires new metrics. Traditional KPIs like CAC or LTV must be adjusted for regional variation.

Key metrics include:

- Regulatory compliance score per market

- Operational efficiency ratio (cost per transaction)

- Time-to-market for new launches

- Customer support resolution times across time zones

- System uptime by region

Dashboards should unify global visibility with local granularity. Sophisticated analytics aren’t a luxury. They’re essential for identifying bottlenecks before they impact customers.

Related post: Best Practices for Remote Staff Management: Succeeding Across Borders

The Rise of Global Fintech Hubs

The globalization of finance is no longer theoretical; it’s physical. Across continents, governments and regulators are creating global fintech hubs designed to attract innovation, capital, and cross-border collaboration.

These hubs have become launchpads for scaling fintech operations worldwide, offering structured ecosystems that reduce friction in regulatory approval, licensing, and market entry.

1. The Modern Fintech Power Triangle: Singapore, London, and Dubai

- United States (especially Silicon Valley, San Francisco, and New York):

The US remains the leading global fintech hub thanks to deep venture capital markets, tech talent, financial expertise, and high fintech investment volumes.

- United Kingdom (notably London):

The UK holds a senior position among global fintech ecosystems, with strong regulatory support, investor confidence, and high concentrations of fintech companies.

- Singapore:

Singapore continues as the premier Asian fintech hub, drawing startups, capital, and regulatory innovation (including sandbox frameworks and regional data sharing).

These hubs serve as strategic springboards. They offer localized regulatory clarity, operational resources, and investor access while enabling rapid multi-market scalability.

2. Emerging Fintech Hubs: Where Growth Is Accelerating

Beyond the “big three,” new global fintech hubs are rapidly gaining traction:

North America

Canada

USA:

South Asia

India

Southeast Asia

Philippines

Thailand

Vietnam

Indonesia

Africa

Kenya

Nigeria

Middle East

UAE

Bahrain

Latin America

Brazil

Europe

Netherlands

Switzerland

Australia

Each hub provides distinct advantages, from regulatory leniency to engineering depth. However, their shared feature is the ability to accelerate scale through ecosystem connectivity.

What Leaders Underestimate About Global Expansion

Even with access to the best fintech hubs and technology, some fintech leaders still stumble when scaling across borders.

The cause is rarely ambition; it’s underestimating how operational complexity multiplies as expansion accelerates.

1. Operational Coordination Is Nonlinear

Each new market adds not just one set of processes but a web of interdependencies: from new payment rails to regional support teams. Managing these layers requires strong orchestration systems, centralized dashboards, and dedicated global operations managers to prevent fragmentation.

2. Compliance Agility Lags Behind Regulation

Regulations evolve faster than systems. Without automated compliance pipelines and globally distributed compliance analysts, companies face escalating delays and audit risks. Successful fintechs now treat compliance like DevOps: continuous, proactive, and measurable.

3. Customer Support Scaling Is More Than Staffing

It’s not just about adding more people; it’s about expanding empathy and localization.

Multi-time-zone support, multilingual service, and local payment knowledge define customer satisfaction in fintech.

This is where EOR and managed operations models shine: they let fintechs scale human coverage efficiently while maintaining training, process consistency, and compliance.

4. Cross-Market Dependencies Ripple Across Systems

Changes in one region, such as AML thresholds or transaction caps, can affect global transaction routing and fraud systems. Fintechs need real-time global oversight to understand how local shifts cascade through shared infrastructure.

5. Workforce and Knowledge Management

As fintechs expand, distributed teams often operate in silos, leading to misalignment and inefficiencies.

Forward-thinking leaders now invest in knowledge continuity programs, shared documentation systems, and cross-border workforce integration. This could be managed through centralized HR and operational partners like CORE®.

Borderless Fintech Operations for Sustainable Scale

The fintech industry has entered a new era: one where innovation alone no longer guarantees success. The leading fintech companies of 2026 aren’t just redefining finance; they’re redefining how to operate globally.

The latest fintech trends reveal that true competitive advantage lies in operational scalability. This is the ability to replicate compliance, customer experience, and transaction reliability across multiple markets without friction.

It’s no longer enough to have a brilliant product; fintechs must now master cross-border payments, fintech compliance, and global workforce orchestration as part of their core strategy.

Frequently Asked Questions (FAQs)

Q1: What are the trends in fintech?

The biggest trends include embedded finance, real-time cross-border payments, AI-driven operations, tokenization and decentralized finance (DeFi) — all reshaping how fintechs scale globally.

Q2. What are the 5 D’s of fintech?

They are Digitization, Data, Decentralization, Disruption, and Democratization — the forces driving fintech innovation.

Q3. What are the 4 pillars of fintech?

The four pillars are Payments, Lending, Wealth Management, and Insurance, which form the foundation of most fintech models.

Q4. What are the biggest operational challenges in fintech global expansion?

Managing compliance across multiple jurisdictions, building scalable cross-border payments infrastructure, and maintaining consistent customer support across time zones and languages.

Q5. How do successful fintech companies manage global operations?

They adopt hybrid models, centralizing risk and compliance while localizing customer support and partnerships. Additionally, these are supported by automation and flexible frameworks.

Q6. What operational systems should be in place before expanding globally?

Cloud-first infrastructure, automated compliance monitoring, multi-currency payment processing, and multilingual customer support systems are essential for resilience.

Q7. Which regions offer the best opportunities for fintech expansion?

Asia-Pacific leads with mobile-first adoption, North America and Europe offer high revenue potential with complex compliance, while Africa and Latin America present emerging opportunities with unique local challenges.

Ready to scale your fintech operations globally?

One CoreDev IT® specializes in helping fintech companies build the operational infrastructure needed for successful international expansion. Our experienced teams understand the complexities of cross-border payments, fintech compliance, and multi-market operations. We provide the remote talent and operational expertise that allows fintech companies to expand confidently while maintaining operational excellence.

Whether you need compliance specialists, risk management experts, or customer support teams that can operate across time zones, we help you build the operational foundation for sustainable global growth.